Table of Content

Pre-qualification is based solely on verbal information you tell a lender about your income and savings, says Valentini. So, it shows how much you could theoretically borrow, but it’s no guarantee—which means these buyers will have to get officially approved for a loan later on and cross their fingers it works out. If you’re in the early stages of the home-buying process, prequalification can help you ballpark your budget. If you don’t prequalify for the loan amounts that you were hoping for, here are a few tips to afford more house. Except for jumbo loans, all loans conform to Fannie Mae and Freddie Mac guidelines. Some loans are designed for low- to moderate-income homebuyers or first-time buyers.

Pre-approval meetings are restricted to hours when the bank is open, and loan officers often require multiple days to review and pre-approve an application. By definition, a pre-qualification is non-reliable as evidence of a buyer’s ability to buy. As a result, sellers don’t accept offers from pre-qualified buyers. For each pre-approval, the lender carries out a hard inquiry that may impact your scores negatively.

What is mortgage loan origination?

View your car’s estimated value, history, recalls and more—all free. Closing day is the day your mortgage is official—and you get the keys to your property! To learn more about relationship-based ads, online behavioral advertising and our privacy practices, please review Bank of America Online Privacy Notice and our Online Privacy FAQs. We strive to provide you with information about products and services you might find interesting and useful. Relationship-based ads and online behavioral advertising help us do that. We ask for your email address so that we can contact you in the event we're unable to reach you by phone.

If that's the case, you'll want to get pre-approved for a mortgage. This is an important step in the homebuying process and can help you save time and money. Mortgage pre-qualification should not be confused with pre-approval.

Is There A Difference Between A Mortgage Pre-Qualification and Pre-Approval?

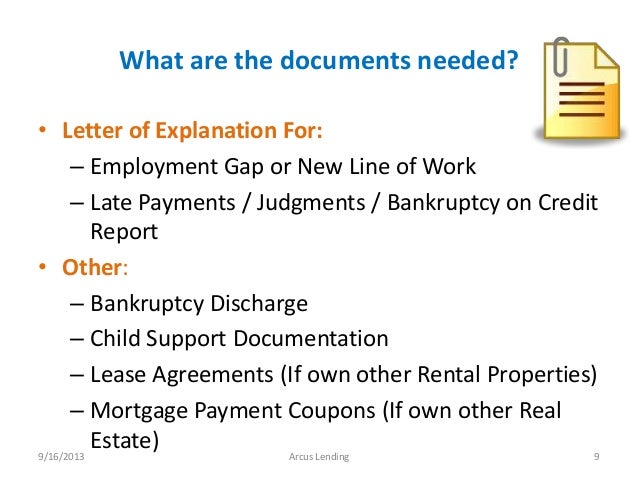

Because a prequalification is an initial review of your finances, you usually don’t need to supply documentation during this stage. If you are pre-approved, your lender will provide you with a pre-approval letter on an official letterhead. This official document indicates to sellers that you’re a serious buyer and verifies that you have the financial means to make good on an offer to purchase their home. Most sellers expect buyers to have a pre-approval letter and will be more willing to negotiate with those who prove that they can obtain financing. If you’re a self-employed borrower, you might be asked to provide additional documents to show a consistent income and work history of at least two years. Some documents requested may include a profit and loss statement, a business license, your accountant’s signed statement, federal tax returns, balance sheets, and bank statements for previous years .

Because it is riskier for the bank to lend money to someone with an unverified income, expect your mortgage interest rate to be higher for a no-documentation loan than for a full-documentation loan. A lender is required by law to provide you with a three-page document called a loan estimate within three business days of receiving your completed mortgage application. Since completing a pre-approval application does affect your credit score, getting a free check that won’t impact your credit will give you a rough idea of your current score. You can then use the estimate as a baseline for checking if you meet a lender’s mortgage qualifications. Lenders might overlook higher debt-to-income ratios if you have other positive factors in your favor.

How to Shop for a Mortgage: A Home Buyer's Guide to the Right Type of Loan

Although you’d be living in the house, their assets would be on the line if you couldn’t keep up with your mortgage payments. That’s because you’ll be able to handle a larger mortgage payment with more money coming in every month. When you improve your credit score, a lender may be willing to increase your preapproval amount. Additionally, a higher credit score may be able to lower your interest rate.

But, once you’re fully approved for a loan, you’re ready to move forward with the closing. A preapproval is not a finalized offer; it’s one step on the path toward approval. One way to think of a preapproval versus an approval is the difference between a mechanic taking a quick look under the hood of your car and a mechanic doing a 100-point inspection. Under federal law, you’re entitled to a free copy of your credit report from each credit bureau once per year.

What does it mean to prequalify for a home loan?

That’s because putting down 20% eliminates private mortgage insurance , which is a cost tacked onto your monthly payments. The lender may increase your preapproval amount without mortgage insurance added to your monthly mortgage. Even if you’re preapproved, it’s possible you could get denied the loan if anything doesn’t check out.

If you’ve had several inquiries, you may see a larger impact on your credit. Will provide you with enough information to confidently continue your home search. Your lender will also have many of the necessary financial and personal information on-hand to be able to process your loan approval once you have a purchase contract in place. Mortgage preapproval can give you an important strategic advantage when you're buying a home in today's red-hot real estate markets. Correct timing of your preapproval application is an important tactic in your homebuying game plan.

Most lenders will demand proof of income, which means tax returns and payroll stubs. On top of all that, you must provide recent bank statements detailing all your assets. If you have a down payment of less than 20%, you will typically be required to pay private mortgage insurance , which increases your monthly mortgage payment. The underwriter will review your documentation to estimate whether you have enough money to cover closing costs. You may also be required to have set aside 2 or more monthly mortgage payments as reserves, depending on the loan program and/or loan amount.

Plus, a preapproval provides additional information to help you prepare for a purchase. You’ll not only receive information about loan terms and loan amounts, but also estimates regarding interest rates, down payment amounts, and monthly mortgage payments. For example, after a review of your prequalification form, a lender might say you prequalify for a mortgage up to $150,000. If you believe you’re able to find a suitable property within this price range, you might proceed with the mortgage application process. But if not, you could postpone the mortgage and wait until your financial situation improves.

Read our top 10 first-time home-buyer tips to help guide you through the process. Benefits of buying a house vs. renting an apartment Deciding to buy a house vs rent an apartment should be based on costs, lifestyle and location. Deciding to buy a home is a significant investment and not one to be taken lightly. Taking time to understand how to put yourself if the best financial position for pre-qualification and approval is an essential first step. Let us help make the buying process easier, allowing you to enjoy the home buying experience. If your debt-to-income ratio is more than 43%, you still may be eligible for a mortgage if another person completes the application with you.

This type of mortgage is based on the income that you report to the lender without formal verification. Stated income loans are sometimes also called low-documentation loans because lenders will verify the sources of your income rather than the actual amount. Most lenders require a FICO Score of 620 or higher to approve a conventional loan, and some even require that score for a Federal Housing Administration loan. If you have not opened credit cards or any traditional lines of credit—such as a car loan or student loan—then you might have trouble getting a mortgage pre-approval.

No comments:

Post a Comment